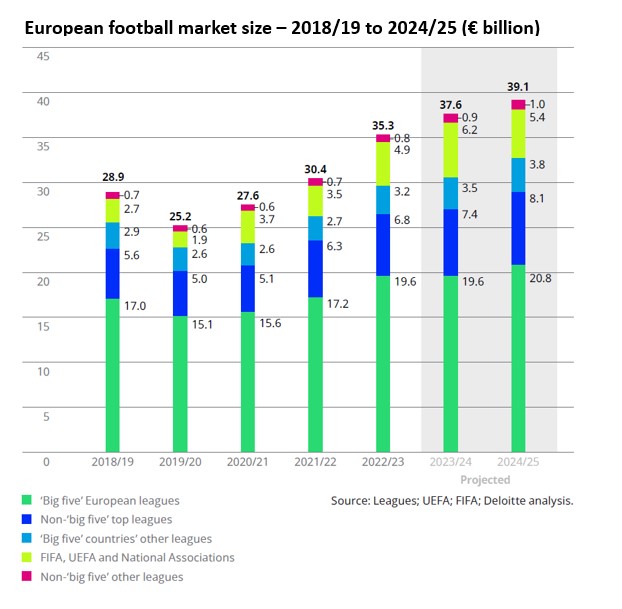

The European football market grew by 16% in the 2022/23 season to €35.3bn, boosted by the lifting of all remaining COVID-19 restrictions and the 2022 FIFA World Cup;

The European football market grew by 16% in the 2022/23 season to €35.3bn, boosted by the lifting of all remaining COVID-19 restrictions and the 2022 FIFA World Cup;- The ‘big five’ European leagues generated total revenue of €19.6bn, up €2.3bn (14%) on the previous season, and reported an aggregate operating profit (€0.5bn) for the first time since 2018/19;

- Premier League clubs’ revenue grew 11% to surpass £6bn for the first time, with average revenue in the English top-flight exceeding £300m;

- With the full return of fans to stadia in Germany and Italy, Bundesliga and Serie A clubs reported the largest proportional revenue growth over the previous season (22% each);

- Championship clubs’ revenue exceeded wage costs for the first time since 2016/17, with total revenue rising by 10% and an average wages/revenue ratio of 94%;

- The Lionesses success at the EUROs supported a 50% growth in Women’s Super League clubs’ revenue, which hit £48m in the 2022/23 season.

Revenue across the European football market grew by 16% to €35.3bn in the 2022/23 season (€30.4bn in 2021/22), according to the 33rd Annual Review of Football Finance published by the Deloitte Sports Business Group. The 2022/23 season played host to the winter 2022 FIFA World Cup and was also the first since 2018/19 unaffected by COVID-19 restrictions.

The ‘big five’ European leagues – the Premier League, Bundesliga, LaLiga, Serie A and Ligue 1 – saw revenue growth of 14% to total €19.6bn, driven by an uptick in matchday revenue, new and improved sponsorship deals, and the utilisation of stadia beyond matchdays.

The Premier League once again dominated financially across Europe in the 2022/23 season, with clubs in the English top-flight registering aggregate revenue of £6.1bn – an 11% increase on the previous year (£5.5bn).

This record-breaking season sees the league surpass the £6bn revenue mark for the first time, driven by a 14% rise in matchday revenue (£867m), as a new record average league attendance was set, alongside a £221m year-on-year increase in commercial revenue (to £2bn) and a 9% uptick in broadcast revenue (to £3.2bn).

Total wage costs in the Premier League increased by 10% to surpass £4bn for the first time. However, despite annual growth in wages (£377m) being lower than growth in revenue (£603m), rising wage costs and amortisation adversely impacted pre-tax losses in the Premier League, which increased by 14% to £685m.

Overall, Premier League clubs’ operating profits (excluding player trading) fell by 18% to £393m, as other operating expenses increased to c.£1.6 billion, driven in part by inflation. Net debt of clubs in 2022/23 rose from £2.7bn to £3.1bn (up £473m), largely driven by funding for infrastructure projects.

While revenues in the Premier League hit new heights, clubs in the Bundesliga and Serie A recorded the largest average percentage growth over the previous season (22%), due in part to the full return of fans to stadia in Germany and Italy.

Bundesliga clubs generated total revenue of €3.8bn in the 2022/23 season (€3.1bn in 2021/22), as matchday nearly doubled to €0.5bn, with Bundesliga clubs reporting the highest average attendance among the ‘big five’ leagues.

Meanwhile, aggregate broadcast revenue for Bundesliga clubs grew by 10% to €1.5bn, largely driven by the stronger performance of German clubs in the UEFA Champions League.

LaLiga also broke records in 2022/23 with the clubs achieving aggregate revenues of €3.5bn. An 8% decrease in aggregate broadcast revenue, largely attributed to weaker performance in European competition across the season, was more than offset by improved matchday revenue (up 32% / €131m) and commercial revenue (up 29% / €274m).

Serie A club revenue totalled €2.9bn in the 2022/23 season, marking a record for the league and a 22% increase on the previous season. Matchday revenue rose by 88% (to €434m), broadcast revenue by 15% (to €1.5bn) and commercial revenue by 14% (to €0.9bn).

Despite a small reduction in aggregate broadcast revenue (down 3% to €0.7bn) and muted growth in matchday and commercial revenue, Ligue 1 clubs’ aggregate revenue also grew by 17% to €2.4bn.

Overall, clubs in the ‘big five’ reported an aggregate operating profit (€0.5bn) for the first time since 2018/19, with the average wages/revenue ratio falling across all leagues.This was due to the substantial increase in aggregate revenue (€2.3bn) exceeding clubs’ increased wage costs (up €0.7bn).

Tim Bridge, lead partner in Deloitte’s Sports Business Group, said: “The 2022 FIFA World Cup, the lifting of final COVID-19 restrictions, and the fervour of fans engaging with football has led to strong growth in the European football market in 2022/23.

“As plans and conversations continue across leagues in terms of further regulation and investment, European football is sitting at an inflection point. Football is growing into an ever more globally connected game, and this brings new challenges to maintaining competitive balance, strong governance and regulation. Leaders across the industry must provide a united front in following good governance principles to build a future for European football that fans, players, and partners across leagues can be excited for.”

The English Football League (EFL), consisting of the Championship, League One and League Two, registered aggregate revenue of £1.1bn in the 2022/23 season.

Championship clubs recorded total revenue of £749m in the 2022/23 season, a 10% increase (from £678m) compared to 2021/22. This was largely a result of the club mix, with five clubs in receipt of parachute payments contributing an aggregate of around £200m (27%) of the league’s total revenue.

Championship club revenues exceeded wage costs (£706m) for the first time since 2016/17, with a wage/revenue ratio of 94%. However, the second-tier clubs remained heavily loss making as the league registered operating losses of £316m, with no single Championship club generating an operating profit (before player trading).

Overall revenue growth in the Championship was supported by a 21% uplift in commercial revenue, to £199m, and a 17% uplift in matchday revenue to £152m.

Over 10 million cumulative fans attended a Championship match in the 2022/23 season, making it the fifth highest total attended division in Europe behind only the Premier League, Bundesliga, La Liga and Serie A.

Both League One and League Two reported an increase in revenue in 2022/23. League One clubs’ average revenue rose 9% to £9.8m, partly driven by increases in revenue among the league’s consistent clubs.

Meanwhile, League Two clubs’ saw a very marginal 1% rise in average revenue to £5.4m, aided by increased matchday attendances.

In total, 19.8 million cumulative fans attended matches across Championship, League One, and League Two competitions in 2022/23, marking the largest aggregate figure in almost 70 seasons (1953/54).

Bridge concluded: “The Football League may have seen an uptick in revenues in 2022/23, but clubs across the EFL are still battling to manage cash requirements.Many clubs are propped up by owner funding as they aspire to promotion, but exiting the league at the wrong end exposes a club to instability. This makes a strategy for long-term stability critical, underpinned by appropriate support provided by the governing bodies.”

Deloitte’s analysis highlights that Women’s Super League (WSL) clubs generated £48m in aggregate revenue in the 2022/23 season, the first season following the Lionesses’ EURO 2022 triumph, a rise of 50% on 2021/22 (£32m).

The findings show that WSL clubs’ revenue more than doubled over two seasons, with aggregate WSL club revenue standing at £20m in 2020/21. Further growth is predicted, with revenue forecast to reach £52m in the 2023/24 season and to rise to £68m in 2024/25.

Jenny Haskel, knowledge and insight lead in the Deloitte Sports Business Group, said: “Driving a loyal fanbase, habitual viewing, and distinct commercial partnerships was a clear priority for WSL clubs in the 2022/23 season and the soaring revenue growth achieved demonstrates the strides that have been made. However, we’re still in the foothills of growth in the women’s game. As NewCo concentrates on growing the popularity, standards, and visibility of the women’s game in England, collaboration with clubs and other stakeholders will be an important element to continuing the efforts to attract the attention of commercial partners, investors, and crucially, fans.”